The short version: Collin County’s headline number is one thing, but the submarkets are pricing very differently right now. Late May 2026 has the county median near $500K, McKinney near $573K, Frisco near $687K, and Prosper averaging above $979K — with active inventory across the county running about 8% higher than last year. Here is what that means if you are buying, selling, or refinancing this summer.

Collin County snapshot — late May 2026

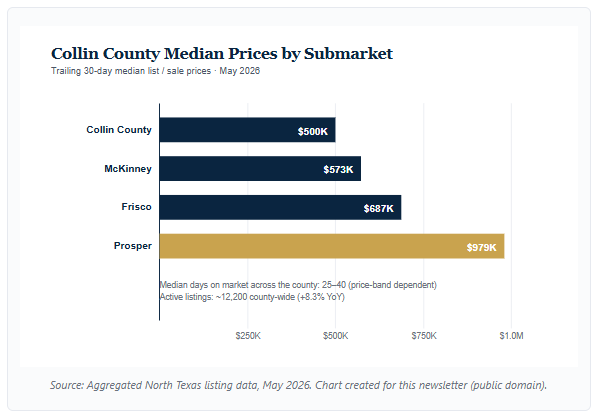

Active inventory across Collin County is hovering near 12,200 homes — roughly 8% higher than this time last year and meaningfully above the long-term average for our area. Median days on market sit in the 25–40 day range depending on submarket and price band. The headline story has not changed materially from the start of May: this is a market where well-priced homes still move, and where overpriced ones sit.

What has changed is the spread between submarkets. The single most useful thing a Collin County buyer or seller can do right now is stop talking about “the Collin County market” and start talking about their specific submarket.

Submarket-by-submarket: what the numbers actually say

Collin County overall (~$500K median list)

The county-wide median list price is hovering around $500,000, down a modest single-digit percentage year over year. This is a useful directional number — but the moment you zoom in on a specific city, the picture changes.

McKinney (~$573K median list)

McKinney is the steadiest story in the county right now. Median list prices are essentially flat year over year, with the market continuing to draw demand from buyers who want walkable historic-downtown character, strong schools, and a slightly slower pace than Frisco. Days on market in McKinney’s mid-tier neighborhoods are tracking close to the county-wide range.

Frisco (~$687K median)

Frisco’s trailing 30-day median is in the high $600Ks, with values bumping slightly higher year over year on the strength of west-side and Phillips Creek Ranch-area inventory. New listings continue to come on at a healthy pace, but the desirable subdivisions are still seeing weekend showing activity and competitive offers when a home is priced correctly out of the gate.

Prosper (~$979K average sale)

Prosper is the price-band outlier. The April average sale price ran near $979,000, with homes transacting at roughly 95% of original list price. The luxury end is being supported in part by out-of-state inflows and by the steady drumbeat of new estate-scale inventory — most notably the Mirabella master-planned community now under construction along Custer Road.

Featured premium development: Mirabella

Highland Homes and Huntington Homes are building Mirabella on a roughly 190-acre site north of Highway 380 in Prosper, with approximately 285 homes planned and pricing expected to start near $1M. The Huntington side will sit on oversized 84- and 100-foot homesites — estate-scale lots that are increasingly hard to find in Collin County’s newer development corridors. First homes are anticipated to be available later in 2026.

Even if you are not in that price band today, Mirabella is the kind of new inventory that resets expectations for what “new construction in Prosper” looks like over the next 12–24 months.

National rate environment

Long-term Treasury yields moved meaningfully higher over the recent holiday week after April’s PCE inflation reading came in at a roughly three-year high. Mortgage pricing tracks the 10-year Treasury more than it tracks the Federal Reserve itself, which is why the bond-market move matters more for borrowers than the Fed’s next decision (currently scheduled for June 16–17).

Pricing changes daily and depends on credit profile, loan size, occupancy, property type, and several other factors, which is exactly why I will not quote a rate in a blog post. What I will say is that this week’s move means the math has shifted slightly for borrowers in active processing — if you have an application open right now, this is a good week to talk to your lender.

Financial markets in plain English

The S&P 500 set another record close mid-week, led by AI and cloud software names. The Russell 2000 outperformed on the week. PCE inflation came in at a three-year high; jobless claims and consumer spending held up; oil prices fell sharply on an extension of the U.S.-Iran ceasefire.

The translation for households is familiar: equity portfolios continue to do constructive work, while borrowing costs are not collapsing. That combination favors families with the flexibility to act when the right house appears rather than the family waiting for a rate that may or may not arrive.

Frequently asked questions

Are home prices in Collin County actually falling?

The county-wide median has softened by a single-digit percentage year over year, but performance varies meaningfully by city. McKinney is essentially flat. Frisco is slightly higher year over year on the trailing 30 days. Prosper’s average sale price remains in the high $900Ks. A pricing decision for a specific home should be based on comps from that specific submarket and price band, not on county-wide averages.

Why is Prosper so much more expensive than the rest of the county?

Prosper has a larger share of estate-scale inventory and continues to draw out-of-state buyers who are looking specifically for larger lots, newer construction, and top-rated schools. The new Mirabella master-planned community along Custer Road is one of several upcoming developments expected to anchor pricing at the $1M-and-above level.

Where are mortgage rates headed?

Forecasting rates with precision is not something a responsible lender does in writing. Rates track the 10-year Treasury, which itself reacts to inflation data, Federal Reserve guidance, and broader economic conditions. The most useful posture for any household is to be ready to move when the personal math works — not to try to time a market that nobody times consistently.

Is now a reasonable time to buy in Collin County?

It depends on the household. Buyers today have negotiating room they did not have in 2021 or 2022 — below-list offers, closing-cost concessions, and temporary rate buydowns are landing in a meaningful share of contracts. The right answer for a specific household depends on their timeline, current rent or mortgage, savings position, and which submarket they are looking in.

Get a clear picture for your situation

If you would like a no-pressure read on what your numbers actually look like — purchase, sale, or refinance — I am happy to put it together for you.

Run a payment check Call 945-300-4644

Wayne Wallace, SVP of Mortgage Solutions at Homewood Mortgage, has spent 27 years helping North Texas families navigate home financing — through every type of market this region has produced. He lives and works in Collin County and publishes The Collin County Briefing weekly for clients, partners, and neighbors.

Homewood Mortgage, LLC · NMLS #294974 · Wayne Wallace NMLS #745186 · Licensed in Texas · This is not a commitment to lend. Equal Housing Opportunity. All loan products are subject to credit and property approval. Information herein is for educational purposes only and is not an offer to lend, investment advice, legal advice, or tax advice. Market data sourced from publicly available real estate and financial reporting and is subject to change.

Ready to Take the Next Step?

Get a free, no-obligation pre-approval in about 15 minutes. I’ll show you exactly what you qualify for in North Texas.

Apply Now — It’s Free Call 945-300-4644

Or see what North Texas homebuyers say about working with Wayne →

Homewood Mortgage, LLC | NMLS #294974 | Wayne Wallace NMLS #745186 | Licensed in Texas | This is not a commitment to lend. Loan approval subject to credit, income, and property qualification. Programs, rates, and terms subject to change without notice.

Homewood Mortgage, LLC · NMLS #294974 · Wayne Wallace NMLS #745186 · Licensed in Texas · This is not a commitment to lend. Equal Housing Opportunity. All loan products are subject to credit and property approval. Information herein is for educational purposes only and is not an offer to lend, investment advice, legal advice, or tax advice. Market data sourced from publicly available real estate and financial reporting and is subject to change.