Collin County’s housing market is handing buyers something they haven’t had in years: options, time, and negotiating power. Here’s the full picture for June 2026.

Collin County Market Snapshot: The Numbers That Matter

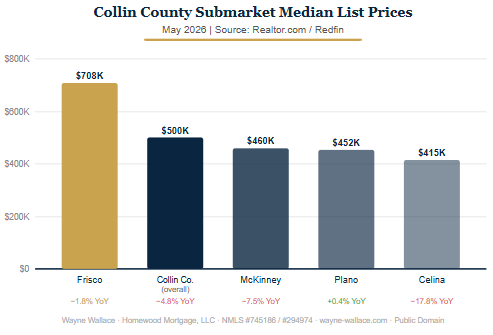

As of late May and early June 2026, Collin County is firmly in transition. Active listings have climbed past 12,244 — up more than 8% year-over-year — and that inventory surge is reshaping how buyers and sellers interact. The median list price has pulled back to $500,000, down nearly 5% from a year ago, while the median sold price sits around $466,875. Homes are spending about 40 days on market on average, and 74% of closed transactions are landing below list price.

That last figure is the one worth pausing on. For the better part of the past three years, sellers in North Texas suburbs held most of the cards. That dynamic has meaningfully shifted. Today, a well-informed buyer — one who’s pre-approved, knows the submarkets, and moves with confidence — is in a genuinely advantageous position.

Submarket Breakdown: Where Opportunity Sits Right Now

Frisco remains the county’s price leader, with a median near $708,000, though even this market has eased — values are down about 1.8% year-over-year. For buyers who want Frisco’s school districts and amenities and have the budget for it, there’s more selection and less urgency-pressure than there’s been in years.

McKinney is one of the more interesting stories in the county right now. Median prices have pulled back toward $460,000 — a roughly 7.5% decline year-over-year — in a city that continues to grow, attracts businesses, and maintains consistently strong quality-of-life rankings. Buyers willing to act in this window may look back on 2026 as a good year to have bought in McKinney.

Plano has shown notable resilience, with median values essentially flat year-over-year — the only major Collin County submarket holding positive. For buyers who prioritize stability and the established amenities Plano offers, that data point matters.

Celina has experienced the most dramatic market correction in the county, with values down roughly 18% from their peak. For buyers who want new construction, generous lot sizes, and room for a growing family — without the Frisco price point — Celina deserves a serious look right now. The fundamentals of the area (growth trajectory, infrastructure investment, school district quality) haven’t changed. The price has.

Prosper continues its evolution into one of North Texas’s premier addresses. The newly announced Mirabella community — a 190-acre gated development from Highland Homes and Tellus Group, with approximately 285 homes expected to start around $1 million — is breaking ground this summer, signaling continued confidence in Prosper’s long-term trajectory even amid broader market softness.

The National Rate Environment: What It Means for Collin County Buyers

The Federal Reserve has remained cautious and data-dependent throughout 2026, in no particular hurry to change its current stance. Inflation has proved stickier than many forecasters hoped, and that’s kept borrowing costs elevated compared to the levels buyers were hoping to see by now. The 10-year Treasury yield — which mortgage pricing closely tracks — has been running at elevated levels, pushed higher by resilient economic growth, energy costs, and an AI-driven capital spending surge that’s added to underlying inflation pressures.

The practical implication for buyers: the rate environment isn’t what anyone wished for, but it is knowable and workable. More importantly, the combination of elevated rates and softened purchase prices — with real negotiating room on the latter — creates a different calculus than buyers faced 18 months ago. A pre-approval conversation clarifies exactly what the numbers look like for your specific situation, and that clarity is worth more than speculation about where rates are headed.

Markets in Plain English: The Broader Economic Picture

U.S. equities have been hitting new milestones this week, with the S&P 500 clearing 7,600 for the first time on the back of strong AI and semiconductor sector performance. Stock market volatility, which spiked earlier this year amid geopolitical and energy price concerns, has settled back below its long-term average — a sign that broader investor confidence has stabilized.

Bond markets have been more turbulent. Treasury yields have risen in response to stronger-than-expected economic growth and persistent inflation, and that pressure has flowed through to long-term borrowing costs. A resilient economy keeps housing demand intact in growth markets like Collin County — but it also means waiting for a dramatic rate improvement may not be a winning strategy.

Frequently Asked Questions

Is Collin County still a good place to buy a home in 2026?

Yes — and in several ways it’s a better time to buy than it has been in recent years. Inventory is up, prices have softened, sellers are negotiating, and buyers have more time to make decisions. The underlying fundamentals of Collin County — job growth, top-ranked school districts, infrastructure investment, and population inflow — remain strong. The short-term price correction doesn’t change the long-term story.

Which Collin County submarket offers the best value for buyers right now?

That depends on your priorities. Celina offers the most dramatic price correction and strong new-construction inventory — ideal for buyers prioritizing space and value. McKinney offers a compelling blend of established community, price softness, and long-term fundamentals. Plano has held its value better than anywhere else in the county and suits buyers prioritizing stability. Frisco and Prosper remain premium markets for those with the budget who want top-tier amenities and newer communities.

How long does it take to get pre-approved for a home in North Texas?

With Homewood Mortgage, most buyers can complete a full pre-approval in about 15 minutes. Having that pre-approval in hand before you start touring homes — especially in a market where negotiation is back — puts you in a meaningfully stronger position. It also helps you shop with confidence, knowing exactly what you qualify for before you fall in love with something.

Should I wait for mortgage rates to come down before buying?

This is the question I hear most often right now, and the honest answer is: maybe, but probably not for as long as most buyers assume. Rates will move when economic conditions warrant it — and no one can predict that timing precisely. What we can control is the purchase price negotiation, which is real and available right now. Many buyers are finding that the combination of current rates plus a well-negotiated price — including seller concessions toward closing costs or rate buydowns — produces a payment they’re comfortable with. A free conversation with me takes 15 minutes and shows you exactly what the numbers look like for your situation. Call 945-300-4644.

Ready to Take the Next Step?

Get a free, no-obligation pre-approval in about 15 minutes. I’ll show you exactly what you qualify for in North Texas.

Apply Now — It’s Free Call 945-300-4644

Or see what North Texas homebuyers say about working with Wayne

Homewood Mortgage, LLC | NMLS #294974 | Wayne Wallace NMLS #745186 | Licensed in Texas | This is not a commitment to lend. Loan approval subject to credit, income, and property qualification. Programs, rates, and terms subject to change without notice.