Understanding Power of Attorney in the Home Loan Process

When buying or refinancing a home, sometimes life’s timing doesn’t line up perfectly. Maybe you’re deployed, traveling, or dealing with a family emergency — but the closing date can’t wait. That’s where a Power of Attorney (POA) can help.

A Power of Attorney is a legal document that lets one person (called the agent) sign important papers and make decisions for another person (the borrower). Fannie Mae allows lenders to accept loans signed using a POA — but only under very specific rules to protect the borrower and ensure the loan remains valid.

When a Power of Attorney Is Allowed

Fannie Mae allows a Power of Attorney to be used for:

- Purchase loans

- Limited cash-out refinances

To qualify, several documentation standards must be met:

- A copy of the POA must be in the loan file.

- Names must match between the POA and the loan documents.

- The POA must be valid and notarized when the loan documents are signed.

- The POA must include the property address.

If local law requires the POA to be recorded along with the deed or security instrument, the lender must ensure it’s done correctly. If an original POA is needed for foreclosure or enforcement, it must be sent to the document custodian.

Who Can and Cannot Act as an Agent

Fannie Mae places tight limits on who can act as an agent under a POA. Unless the person is a relative of the borrower, the following are generally not allowed to sign loan documents as an agent:

- The lender or any of its employees

- The loan originator or anyone affiliated with them

- The title company or its employees (unless an exception applies)

- The seller of the property or anyone connected to the seller

- Any real estate agent with a financial interest in the transaction

A “relative” in this context includes immediate family members, engaged partners, or anyone in a legally recognized relationship with the borrower.

Special Exceptions

There are limited cases when a lender may use a POA signed by someone affiliated with the lender, title company, or other involved party — but strict additional conditions must be met:

- The POA must clearly authorize the agent to sign loan documents for a specific property and specific loan amount.

- The borrower must take part in a recorded online session confirming:

- Their identity

- Their understanding of the loan terms

- Their consent to have the agent sign on their behalf

- The lender must keep a copy of that recording and provide it to Fannie Mae if requested.

- The title insurer must issue a closing protection letter for the transaction (where applicable).

Important Legal Notes

If state or local law requires acceptance of a POA, Fannie Mae’s limits do not apply — but the lender must include a written statement explaining why the POA was accepted under that law.

For trusts, a trustee can only delegate their signing authority through a POA if the trust document specifically allows it or if the borrower is the creator of the trust.

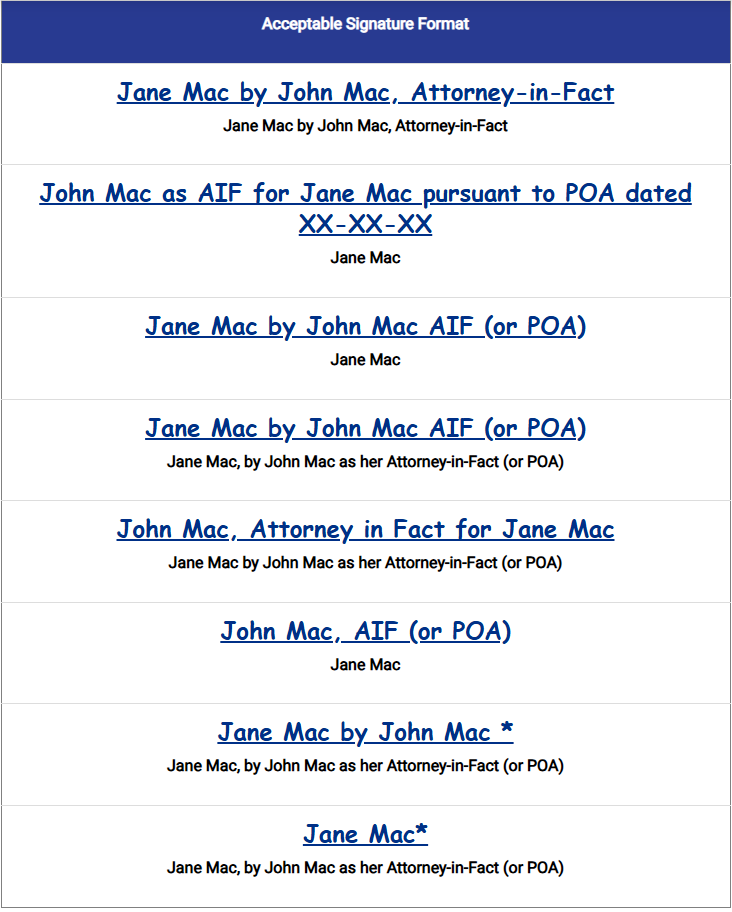

Acceptable Signing Format at Closing

When signing on behalf of a borrower using a POA, the standard accepted format is:

Final Thoughts

A Power of Attorney can be a lifesaver for borrowers who can’t attend closing in person — but it’s critical to do it the right way. Using a POA that doesn’t meet Fannie Mae’s standards could delay your closing or make your loan ineligible for delivery.

If you think you’ll need to use a Power of Attorney in your upcoming home purchase or refinance, talk to your lender early. We can review your situation, make sure your POA is properly structured, and keep your closing on track.

Have Questions About Closing With a POA?

I can review your specific situation, confirm whether a POA is appropriate for your loan, and make sure everything is structured correctly before closing day.

Schedule a 30-Minute Consultation

Wayne Wallace

SVP, Mortgage Solutions | NMLS #745186

Homewood Mortgage, LLC | NMLS #294974

18170 Dallas Pkwy, Ste 304, Dallas, TX 75287

945-300-4644 •

wayne@wayne-wallace.com •

wayne-wallace.com

This content is for educational purposes only and does not constitute legal or financial advice. Power of Attorney requirements vary by state, lender, and loan program. Consult a licensed attorney for legal guidance specific to your situation. All loans subject to underwriting approval. Wayne Wallace, NMLS #745186 • Homewood Mortgage, LLC • NMLS #294974.